Why Inflation?

By Alex Saitta

December 7, 2021

If you can get through this, you’ll know more about inflation and its primary cause than 95% of our elected leaders.

For Example:

Let me give you an example of the way production, price and money all work together. Let’s say our sample economy produces 10 oranges in 2021, the total money supply is $10 dollars, and there are 10 hungry consumers with $1 each. The price of each orange will be $1.

Now let’s say in 2022 the Federal Reserve (the Fed) doubles the money supply so the 10 hungry consumers have $2 each. What happens? Two things. Consumers start to bid up oranges and the price of the fruit rises, AND the rising price entices orange growers to add more orange trees, so they produce 15 oranges in 2022.

What will be the end result? 15 oranges will be sold for an average price of $1.33, when all the $20 of money is spent (15 x $1.33 = $20).

Money printing results in a mix of higher production (GDP) and higher prices (inflation). The politicians hope the mix is favorable — higher GDP growth with little inflation, but it doesn’t always work that way.

Supply Constraints:

Back to our example, what if the farmers are lazy or half stay home because they are getting a government check? What if the regulation costs are high when it comes to adding acreage to farm? What if there is a shortage of labors to pick the oranges?

Back to our example, this time with a twist. Again the Fed doubles the money supply and all the money is spent, but because of these constraints the supply of oranges grows only to 11 oranges. The price of the 11 oranges will be bid up to $1.81 instead. Most of the new money just resulted in price inflation.

The US Economy:

This is roughly what is going on in the US now-a-days. The government is paying people to stay home, it is paying people who are not working, the national work ethic is in a long-term decline, regulation is high, and a variety of other things, so pumping up the money supply doesn’t increase production much. As a result, all this new money chases about the same quantity of goods and services, so prices rise a lot (inflation).

Federal Reserve:

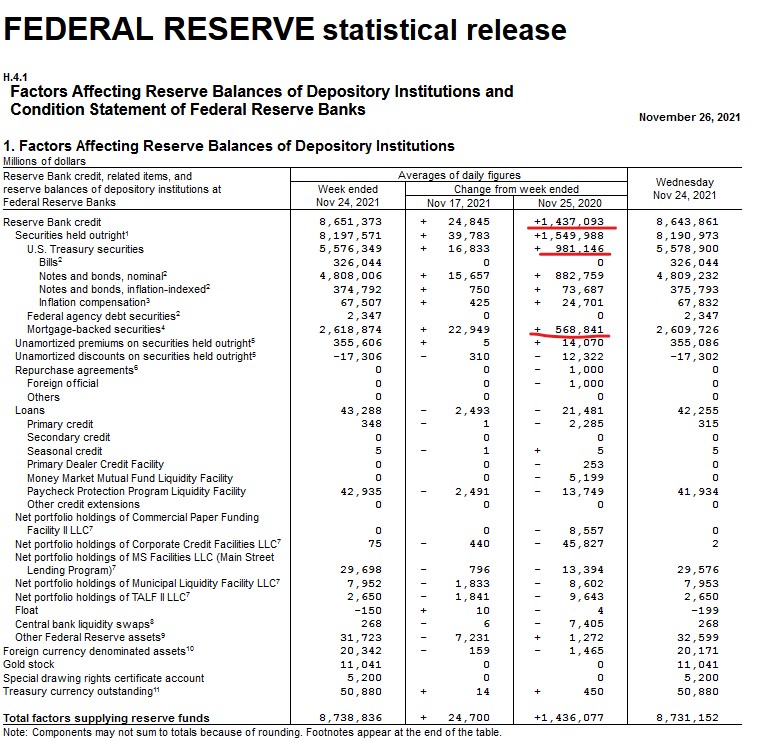

Here is some real, back of the envelope math. Looking at the Fed’s assets, the past year assets grew from $7.2 trillion to $8.6 trillion or an increase of $1.4 trillion or about 19%. See picture — that first underline. Whenever the Fed buys an asset, it creates money. If the Fed bought my house in Liberty for $200,000, the house would show up on its balance sheet tomorrow, and $200,000 would be added to my account. The Fed has no cash, so it would NOT be a transfer of cash into my account, but an electronic addition to my balance. That is how they print money — electronically adding zeros to an account(s).

Unlike in my example, the Fed does not deal with the public directly, only banks that are part of the Federal Reserve System. The Fed buys US Treasury bills, notes and bonds or mortgages that those banks own. Going back to the first picture above — lines 2 and 3, the past year the Fed bought $981 billion in US Treasuries and $568 billion in mortgages from member banks. That is, the Fed created electronically out of thin air $1.4 trillion in reserves at those banks. Those bank reserves become money supply if the banks lend that money out to the public. (I know this skips over a few things; I know about reserve ratios and multipliers, but I’m keeping this basic.)

Looking at the chart below, you can see a graph of the annual percentage change in money supply known as M2. In the year that followed COVID-19, the Fed and member banks grew money supply more than 25%. Right now money supply is growing about 12% annually.

Inflation vs Production:

Thinking back to our oranges example, if money supply is growing 12%, output or GDP is up 3%, the rest is going to result in about 9% inflation annually. (I know about the velocity of money and the percentages are probably off, but I’m keeping it basic here.) To lower inflation, the Fed/ banks either: a) slow the growth of money supply, or b) get GDP production up. GDP growth in good times is restrained to about 3% a year. If money growth is 5%, you’ll have about 2% inflation. That’s ideal.

The current obstacle to that is, the Fed can’t slow money growth to 5% to 6% a year, because the US Treasury borrows so much, interest rates would then rise and crash our debt latent economy.

US Treasury Borrowing:

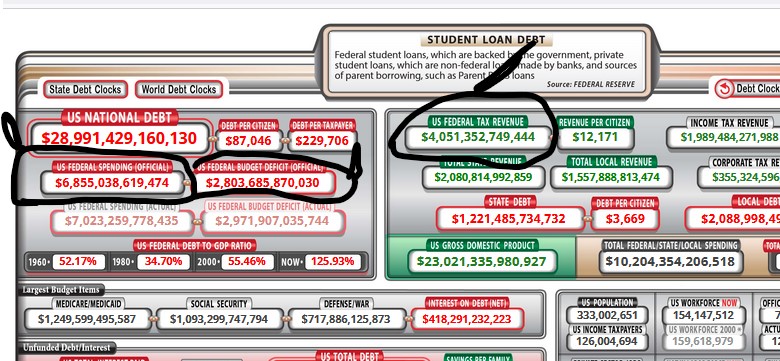

US government revenue is about $4 trillion, expenses are $6.8 trillion and it borrows $2.8 trillion a year to plug the gap (see picture below). When you talk about the 800 pound gorilla in the room, it is the US Treasury in the debt markets. The Treasury borrows a huge amount. As a result, the cost of that money (interest rate) wants to rise response to all their borrowing.

The transaction looks something like this. The US Treasury needs to borrow. ABC, XYZ and LMNOP banks each have $100 extra in their vaults, so they lend the Treasury $100 each or $300 in total. In return the Treasury gives each of the three banks a $100 IOU or bond, with the promise to pay 1.5% interest on the $100 loan each year.

The next week the Treasury is back at it again, looking to borrow. Now the banks have no extra cash to lend. To attract other lenders to lend, the Treasury has to offer a higher interest rate. Each week the Treasury goes to the market to borrow more, in time the lenders become satisfied and interest rates must rise even more in order to draw out additional lenders/ funds. Rising interest rates weigh on individuals, corporations and government which are up to their eyeballs in debt. Some start to default and the then the economy collapses. Our leaders can not allow this to happen, so the Fed steps in.

After ABC, XYZ and LMNOP banks lend $100 each to the US Treasury and the banks are holding their 1.5% yielding T-Bonds, the Fed calls the banks and asks if they want to sell those bonds? The Fed offers to pay them $101 for the T-Bond they paid $100 for. The banks sell those bonds to the Fed and each bank receives $101 from the Fed electronically in their accounts the next day, ready to re-lend to the US Treasury or someone else.

Above I showed you the Fed bought $981 billion in US Treasury securities last year. I just described the shell game they are playing. The government borrows and sells bonds; the banks buy they bonds; the government then buys those bonds back with printed money. The Fed buys up Treasury bonds, bills, notes with a regular injection of new money that keeps interest rates from rising. However, all this new money supply growth, as I illustrated above in the oranges example, creates inflation.

You see the impossible dilemma our leaders have put themselves in. They must keep interest rates low, and to do that they have to buy up oodles of Treasury debt and do it with printed money. All that printed money in the face of low production, results in more inflation. Wages aren’t rising that much, so on a real basis people are falling behind and standards of living are starting to fall.

Hyperinflation:

I was asked about hyperinflation and the chances of that. By definition hyperinflation is an inflation rate of 50% or more a year. To get that, the Fed/banks will have to grow money supply 50% plus a year. They had a 25% growth rate over the 12 months following Covid-19. Money supply is growing about 12% a year now. 50% would be outright banana republic, and would have to be a dire and desperate situation.

The other way we could see hyperinflation is the dollar loses is status as a reserve currency (a long story), the dollar plummets and import prices skyrocket. We import a lot, so inflation would increase an awful amount if the dollar lost its status as a reserve currency.

Conclusion:

Now how do you protect yourself? I knew this was coming and have been talking about it 10 years. Remember me writing a million times, wages are rising 3%, but true inflation is 5 or 6%, so on a real basis the Average Joe is losing 2 to 3% a year of purchasing power each year. Those living hand to mouth are going to get squeezed the most.

I bought precious metals and real estate as a hedge, thinking both would rise with inflation. I was right on real estate and wrong on precious metals. Knowing or suspecting what will happen is often not enough. You have to pick the right investments too, and I really didn’t. Never in a million years did I think stocks or crypto currency would prove to be inflation hedges.

Now what? As I said, our leaders have painted themselves into a corner. This situation will continue to get worse — disappointing economic growth, higher inflation until some of the wheels wobble off. I’m sticking to my guns — real estate, metals and I’ll take another dive into commodities. I am staying away from stocks, bonds, collectables and things like crypto currencies.